By LEWIS JOHNSON – Co-Chief Investment Officer | June 1, 2016 “Poverty is the parent of revolution and crime.”

– John Maynard Keynes

– Aristotle’s Politics

Overindebtedness is the Most Important Issue of Our Time

These pages have for more than two years now chronicled our attempts to distill the elixir of simplicity from the muddy turbulence of an increasingly complex world. We seek to ask the right questions to move further down this path. The most clarifying question we can ask is: 100 years from now, when today’s events are a few sentences in some bored student’s textbook, how will it read? What kernel of truth will have stood the clarifying test of time to reveal, at last, the underlying simplicity of today’s events? We would hazard a guess that overindebtedness will be at the center of that narrative, the struggle of how the world dealt with the challenge of its ubiquitous problem of too much debt.

Perhaps future historians will puzzle the most over why today’s financial regulators so long persisted in the obviously self-defeating delusion that more debt growth could possibly “solve” an overindebtedness problem. Certainly this contradiction seems blatantly obvious to us. Oftentimes the simplest insights are the most profound.

Local Debt Problems are Unlikely to Remain Isolated for Long

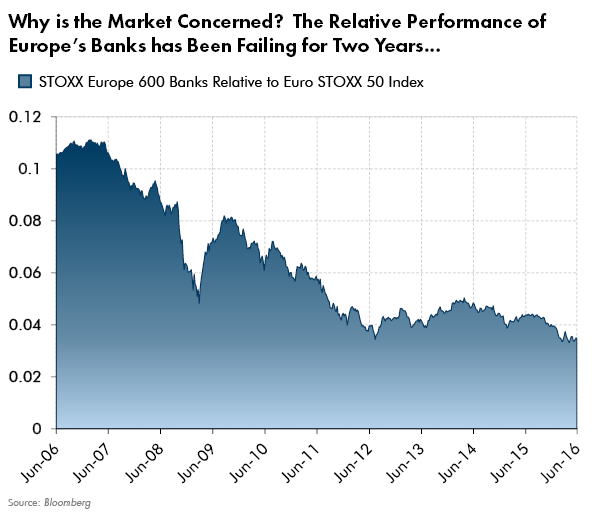

We cannot ignore problems beyond our shores. Our overindebted world is far too connected for that through a complex chain of interlinked debts, as one person’s asset is another person’s liability. Banks act as depositories and clearing houses for these debts, often holding outsized portfolios of assets and liabilities financed with tremendous leverage. Thus are these banks subject to huge potential swings in their fortunes even from the most innocuous changes in prices. These linkages between banks’ balance sheets do not respect borders. As always, in any chain it is the weak link that breaks. So, to profitably navigate an overindebted world, we seek to identify and understand the world’s weak links. Does the relatively weak share price performance of European banks stocks (shown below) justify a closer look? We believe that the answer is yes.

We have been closely monitoring the weakening position of Europe’s banks since 2010. These pages first turned their attention to a deep study of Greece in May of 2014 (“Big Problems Start Small”, May 21, 2014). As our concern about global overindebtedness mounted, we extended our research into China (“The Dark Side of China”, September 24, 2014; “Memory Lane: Chinese Currency Devaluation, August 12, 2015; “China Deflationary Wildcard: Lessons From the Past”, January 13, 2016) , the U.S. Oil Patch (Crude Oil’s Black Friday, December 3, 2014), and now sadly once again back to the Old World. Our eye is now fixed uncomfortably upon Spain.

We have been closely monitoring the weakening position of Europe’s banks since 2010. These pages first turned their attention to a deep study of Greece in May of 2014 (“Big Problems Start Small”, May 21, 2014). As our concern about global overindebtedness mounted, we extended our research into China (“The Dark Side of China”, September 24, 2014; “Memory Lane: Chinese Currency Devaluation, August 12, 2015; “China Deflationary Wildcard: Lessons From the Past”, January 13, 2016) , the U.S. Oil Patch (Crude Oil’s Black Friday, December 3, 2014), and now sadly once again back to the Old World. Our eye is now fixed uncomfortably upon Spain.

Long-time readers know that we seek to be specialists in that which is important. Spain deserves our attention now. But before we outline what we find troubling in Spain, we think it helpful to quickly recount Greece’s financial problems as a potential precedent to what may transpire in Spain.

In Greece, Big Problems Started Small. Political Unrest Made it Much Worse.

Long time readers will recall that in May of 2014 these pages began to chronicle what became the slow- motion meltdown of Greece’s financial system. Key to our thesis was the political blow back we feared as the country’s voters got their first chance to weigh in on the terms of Greece’s bailout. We believed that voters would throw their support to the more radical, anti-austerity parties and this would lead to rising political unrest. We feared that this combination of events could be sufficiently negative to derail what was then a nascent recovery. Sadly, these fears were realized.

Greek voters rejected the harsh terms of austerity that were thrust upon the country by the Troika – the European Central Bank (ECB), the European Commission, and the IMF. Moderate voices in Greece were overwhelmed by the rise of more extreme parties. This rising political uncertainty led investors to question the stability of Greece’s bailout terms, which led to falling government bond prices. This further undermined Greece’s banks, whose portfolios were choking upon these falling bond values. Remember that banks hold bonds as “safe” reserve assets. Accordingly, in a mark to market world, bank depositors can reasonably question their bank’s solvency as they watch the value of these bonds depreciate.

Greek depositors, who were understandably concerned about the increasing fragility of Greek banks, moved their money elsewhere. Capital flowed out of Greece. The European Central Bank became the last remaining source of liquidity to Greece’s troubled banks. Eventually conflict arose between, on one side, Greece’s fed up and angry voters and, on the other side, the Troika and especially the ECB whose tenuous lifeline was the only thing keeping Greek banks liquid and open.

The trickle of capital flight turned into a flood. A full-fledged run began on Greek banks in the summer of 2015 when Reuters reported that “the ECB told Euro zone finance ministers it was not sure if Greek banks would be able to open on Monday.” Panic ensued. Banks were closed. Depositors were denied access to money they had in the bank. The streets erupted into riots. The Troika’s harsh bailout terms were pressed down upon the peoples’ unwilling heads.

Is Spain Following the Path of Greece? Might Spain’s Debt and Bank Problems Spread?

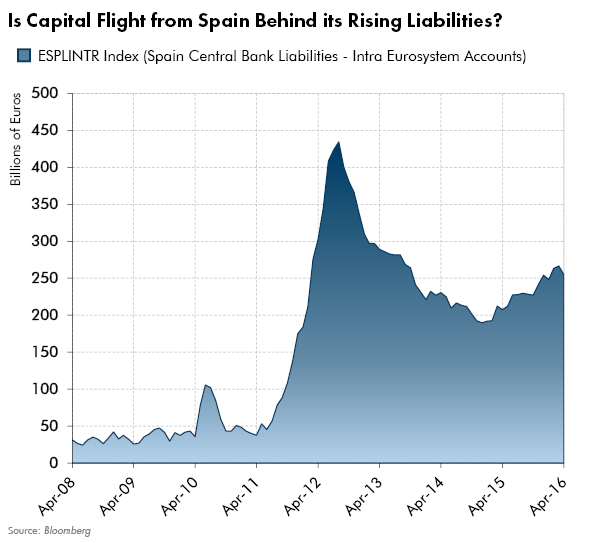

The chart below is one of the more troubling ones that we monitor. It shows that since early 2014 the net indebtedness of Spain’s central bank has grown relative to Euro system accounts. In other words, it’s a measure that suggests to us that Spanish depositors may be transferring money out of the country as they grow fearful about the safety of Spanish banks.

Equally concerning we noted this week the massively dilutive capital raise of Banco Popular Espanol (POP SM in Bloomberg) when the bank almost doubled its shares outstanding by selling two billion shares at a more than 40% discount to its then current share price. The stock plummeted almost 35% in three days. The company’s announced goal was to strengthen its balance sheet. But why the rush? Only days before the company’s outlook had been benign and confident. Is there more to this than meets the eye? Warren Buffett cautions us that there is never just one cockroach. Is management concerned about Spain’s upcoming elections? Time will tell. But we admit that it is with great apprehension that we await Spain’s upcoming elections scheduled for the 26th of June.

Equally concerning we noted this week the massively dilutive capital raise of Banco Popular Espanol (POP SM in Bloomberg) when the bank almost doubled its shares outstanding by selling two billion shares at a more than 40% discount to its then current share price. The stock plummeted almost 35% in three days. The company’s announced goal was to strengthen its balance sheet. But why the rush? Only days before the company’s outlook had been benign and confident. Is there more to this than meets the eye? Warren Buffett cautions us that there is never just one cockroach. Is management concerned about Spain’s upcoming elections? Time will tell. But we admit that it is with great apprehension that we await Spain’s upcoming elections scheduled for the 26th of June.

No one knows the future. Greece’s past need not be Spain’s prologue. But that is our concern. We have seen this familiar pattern unfold through our deep study of Greece. Now, perhaps, that knowledge may help us to understand Spain. In fact, our deepest concern is that the Greek tragedy may repeat itself in time across Europe – Spain, Italy, even France. We can envision a scenario in which bank depositors get frightened into action, with deeply disturbing consequences. The mechanism is the same, only the magnitude of the potential problem is different, each one more disturbing than the one before. Honestly, however, these concerns are not new. In fact, these concerns have darkened our thoughts since Greece first blew up in 2010. That was a long time ago. So far, thankfully, only Greece and tiny Cyprus have succumbed to what is, so far, the worst case scenario.

Europe’s Banks: Reflexivity Squared – Perhaps Even Cubed?

Compounding our concerns are lessons learned from the study of George Soros’ “Alchemy of Finance,” where Mr. Soros outlines his theory of reflexivity. This theory describes the behavior of what Mr. Soros calls “far from equilibrium” events where weakness may trigger more weakness in a self-reinforcing and self-referential cycle. Frankly, in our entire investing career, we have never seen a situation more pregnant with reflexivity: highly leveraged European banks, with local sovereign debt as a reserve; and, sovereign governments who – due to the rules of the Euro – are unable to print money to backstop their financial systems. This is an accident waiting to happen.

No sane person would have concocted this toxic witch’s brew. Europe’s financial regulators may well face the damning verdict of history for what may follow from their lack of vision. We hope that our concerns are misplaced. However, we have learned through long experience not to ignore the power of reflexivity in its ability to drive extreme outcomes.

In Conclusion

Greece has shown how a bad and potentially reflexive situation can become amazingly worse. Elections were an important catalyst for Greece along its descent into the chaos of bank runs. Surely thoughtful observers will be watching closely for the outcome of Spain’s June 26th elections. Past does not have to be prologue. Still, we could not call ourselves diligent stewards of capital if we ignored the precedent of Greece. Furthermore, we must consider that today’s markets are global. Would the share price of U.S. banks blithely ignore rising counterparty risks from troubled European banks? This is another key reason why we reduced exposure to the banking sector a number of months ago.

Spain’s upcoming elections will hold important insights. Will Spain follow in the steps of Greece? One is an anomaly but two is a trend. If so, Spain would present us with a troubling indication indeed that a new trend is growing, that big problems did start small in Greece almost two years ago and are still growing. The dangers of global overindebtedness continue to vex our world. Let us hope that the verdict of history does not find us wanting.