By LEWIS JOHNSON – Co-Chief Investment Officer | June 15, 2016 “France and Great Britain shall no longer be two nations, but one Franco-British Union. The constitution of the Union will provide for joint organs of defense, foreign, financial and economic policies. Every citizen of France will enjoy immediately citizenship of Great Britain, every British subject will become a citizen of France. “

? Neil Sedaka

? Proposal from England’s War Cabinet to France in May of 1940 in the hope of keeping France fighting the Nazi invasion

We cannot shake Orwell’s haunting comments from 1984 that “The end was contained in the beginning.” Somehow it strikes us as foreboding when we contemplate the upcoming English referendum (called “Brexit” by the media) on whether or not England should leave the European Union (EU). Will the EU’s end be contained in its beginning? Is it time to think more expansively about how far the cycle may run – in the opposite direction – from the near complete unification now manifest in the existing EU to what may come after?

In our experience, cycles generally overshoot from one extreme to the other. “Thinking the unthinkable” is often the hardest exercise of all in cyclical investing. If the EU’s intellectual genesis was forged in armed conflict, could a vote to leave the EU set in motion a cycle that may, in the fullness of time, complete the cycle and result once again in armed conflict? Surely, that possibility seems laughable – for now. But the ability to ask seemingly radical questions and consider their answers with an open mind are hallmarks of the best investors.

Europe has been at peace for decades. Each major step it has taken in the last 70 years has been to draw its countries ever more closely together. After all, this referendum is, on the surface, nothing more than a simple vote with thoughtful people disagreeing on both sides of a contentious issue. However, we have been watching events in Europe for many years now, and are disturbed at the ever more contentious arguments in the split between Germany and the creditor powers versus the weaker debtor nations in Europe’s south. Angry debtor countries, such as Greece and Spain, feel oppressed by harsh austerity forced upon them by German-led creditors, and are dredging up the darkest memories from World War II. Greece even reactivated an old claim that Germany owed it war-related reparations numbering in the hundreds of billions of Euros. These are painful memories that go deep. They threaten to reawaken long-simmering animosity on the continent. European peace may be more fragile than it appears.

Will events underway mark a trend change in the almost 70 years of European peace and integration? The long, implacable sweep of history has a way of surprising us all, and taking us to places that we never expected. Who knows, when the future of ongoing events has become the written past, maybe textbooks will date as the inflection point that led to the next conflict these votes in England and Spain taking place this month? Stranger things have happened.

No One is Discussing the Real Issue

Those in the “leave” or “Brexit” camp are in the headlines citing a long list of understandable issues: economic underachievement, immigration, lack of transparent democratic processes; frustration with challenges seemingly beyond the control of local governments. They fail, however, to mention the real issue that is a risk to today’s financial markets.

The real issue should be known to Europe’s politicians and especially understood by its central bankers. The real issue is debt and how its tentacles spread throughout Europe and indeed the world. The Euro as a currency is not just flawed; it’s also the financial equivalent of a thermonuclear debt bomb. Its many and terrible design failures make it dangerous. Its designers and defenders either don’t want to acknowledge its shortcomings or, even worse, are simply unaware of them. Let us explain.

Europe’s banks are bigger, more leveraged, and more indebted than U.S. banks. This means a smaller cushion to guard against unexpected losses. Furthermore, the EU’s fragile financial system of massively overleveraged banks is choking on cross-border liabilities from other banks in a way that almost no one can truly quantify and even fewer understand. Further complicating this issue, the governments that have borrowed in Euros are not free to print Euros to backstop their own banks. Our concern is that this terrible flaw could spread far beyond the limited and understandable issues that divide Britain’s voters. As we have argued many times (“Is Spain the Next Greece?” June 1st 2016), those countries with currencies pegged to the Euro are most at risk from its design flaws – Spain, Italy, and France, just to name a few. But the debts of these countries’ banks to other banks, and frankly the debts of those banks to others, create the preconditions of systemic weakness not seen since the days after Lehman Brothers failed.

The Dangers of Reflexivity: Undercapitalized Banks Backed by Weak Sovereign Governments

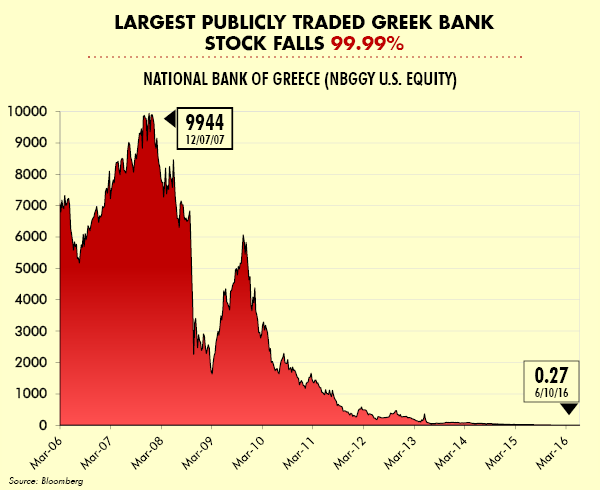

Since May of 2014 (“Big Problems Start Small” May 21st 2014; “Market Raids and Weak Links” October 22nd 2014; “Greece: The Bank’s Problem?” February 11th 2015; “Contagion” May 13th 2015; “Contagion Revisited” July 1st 2015; “Contagion: Fog of War?” July 8th 2015; “Greece: War of Creditors vs. Debtors” July 15th 2015), we have been warning about the flaws in the Eurozone’s design, stemming in part from growing political radicalization, particularly in Greece, as the first major test case for major debt failure within a country that uses the Euro as a currency. Greece is an example of the Euro’s dangers. Greece has suffered capital flight, bank runs, bank closures, capital controls and the forced recapitalization of Greek banks at heartbreaking prices. Amazingly, the price of the National Bank of Greece, the country’s largest bank, has fallen 99.99%, as the chart below demonstrates. Shareholders have been wiped out. Is there a cautionary lesson here for the shareholders of other European banks?

England, by keeping its own currency, the Pound, has avoided the biggest flaw of the Eurozone. The real issue is not whether England votes to stay or go. The real issue is what happens to those countries, such as Spain, Italy, or France, that no longer have their own currencies but rather have adopted the Euro. Their elections are coming up. Is this why the index below of Italian bank stocks is so weak – falling 48% in the last year? Could Italy’s banks follow the pattern of those in Greece? No one knows for sure. Our motto is simple: panic early, beat the rush.

England, by keeping its own currency, the Pound, has avoided the biggest flaw of the Eurozone. The real issue is not whether England votes to stay or go. The real issue is what happens to those countries, such as Spain, Italy, or France, that no longer have their own currencies but rather have adopted the Euro. Their elections are coming up. Is this why the index below of Italian bank stocks is so weak – falling 48% in the last year? Could Italy’s banks follow the pattern of those in Greece? No one knows for sure. Our motto is simple: panic early, beat the rush.

There is a dynamic, which George Soros calls “reflexivity,” that can take a small problem and make it a large problem, should events follow a certain path. Thankfully, the odds are low that weakness in Europe must follow such a dangerously reflexive path. The key to reflexivity is that such events are low in probability but they are high in expected value. Like a game of Russian Roulette with one bullet among the six chambers, the odds are “only” 1/6 that the bullet may be in the unlucky chamber, but the outcome of those low odds is nonetheless catastrophic.

There is a dynamic, which George Soros calls “reflexivity,” that can take a small problem and make it a large problem, should events follow a certain path. Thankfully, the odds are low that weakness in Europe must follow such a dangerously reflexive path. The key to reflexivity is that such events are low in probability but they are high in expected value. Like a game of Russian Roulette with one bullet among the six chambers, the odds are “only” 1/6 that the bullet may be in the unlucky chamber, but the outcome of those low odds is nonetheless catastrophic.

No Bank That is Too Big to Fail Has Been Allowed to Fail Since Lehman. Will That Streak End in Europe?

The Global Financial Crisis of 2008 revealed to the world the incredible complexity and leverage behind the world’s current banking system. Our concern is that: should those countries pegged to the Euro start to seriously consider reverting back to old currencies and leaving the Euro – for whatever reason – we could see the market’s doubts about these countries’ liabilities quickly mushroom into a debilitating wave of forced liquidation and deflation. Once this process starts, it could prove very difficult to control. Sovereign countries who have adopted the Euro as a currency cannot print Euros to bail out their banking systems. This could result in a bank that is indeed too big to fail, failing nonetheless. No one should underestimate the damage that could follow such a decision in today’s overindebted world. This has been chief among our concerns since 2010.

In Greece from 2014 to 2015, we got a taste of what just the threat of these events could entail: rising sovereign bond yields and plummeting bond prices; rising political unrest and anti-Eurozone sentiment; capital flight; banking distress; and, economic downturn. We began to chronicle the events taking place in Greece from May of 2014 onward, before the market understood the danger we saw in the rise of extremist Greek politicians.

Events culminated in a Greek banking crisis, bank runs, closed banks, and finally the forced recapitalization of Greece’s banks from massively dilutive capital raises. We published on this topic months before the market began to focus on the risks in Greece. We did so because we were concerned that, if Greece could have such problems, why couldn’t other countries using the Euro suffer them as well? Was that time invested in understanding Greece well spent? We believe that the answer is yes. Have we learned lessons that apply to Spain and Italy today? We believe the answer is also yes.

We can make out the outline of looming political unrest that may prove to be toxic to the status quo of the Euro. Right now its epicenter is London. Its focus: Brexit. This is all over the news but make no mistake: it’s a sideshow. Pay attention to the real events of that week; the elections in Spain and Italy. There the stage is set for contagion.

In Conclusion

We are always worried about something. There is always some threat that must be addressed, analyzed, and decided upon: to act or not to act. And if we do act, how best to do so? It’s a tiresome exercise. The never-ending contemplation of what might go wrong, what steps we can take to keep clients safe. The investor’s lot is to face a new challenge every day. Some challenges may never materialize; some may fade away; and, still others may begin small and grow into dominant themes that could drive global markets.

We believe that now is the time for thoughtful investors to be on guard. We should not underestimate the events unfolding in Europe. Much may yet depend on their outcome.